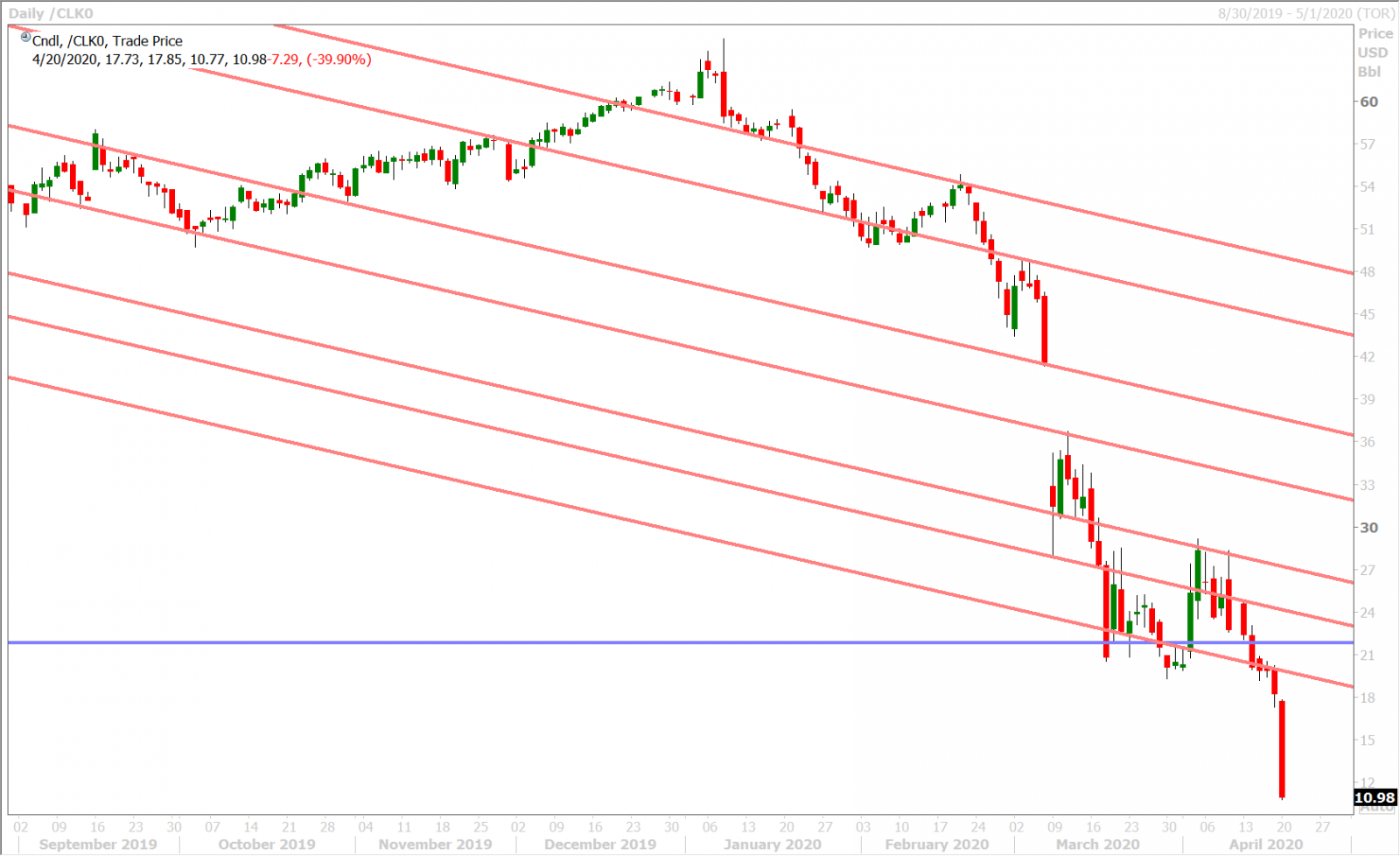

May WTI crashes 40% as nobody wants to take delivery

Interested in creating a custom foreign exchange trading plan? Contact us or call EBC's trading desk directly at 1-888-729-9716.

Get real-time market coverage on twitter at @EBCTradeDesk or sign up here.

SUMMARY

- Physical oil traders, without access to storage, capitulating ahead of May futures expiry.

- May WTI -40%. June WTI -12%. USDCAD regains 1.4100. S&P futures -2%. USD bid.

- EURUSD range-bound but 4th weekly increase in fund net long position doesn’t help bulls.

- GBPUSD testing lower bounds of 1.2430-1.2520s range. Large EURGBP expiry could support.

- AUD enjoying relative strength on talk of New Zealand economic re-opening next week.

- April flash PMI data + EU Summit in focus this Thursday. RBA’s Lowe to speak at 1amET tomorrow.

- USDJPY trading with broader USD tone this morning, inverse correlation to risk sentiment.

ANALYSIS

USDCAD

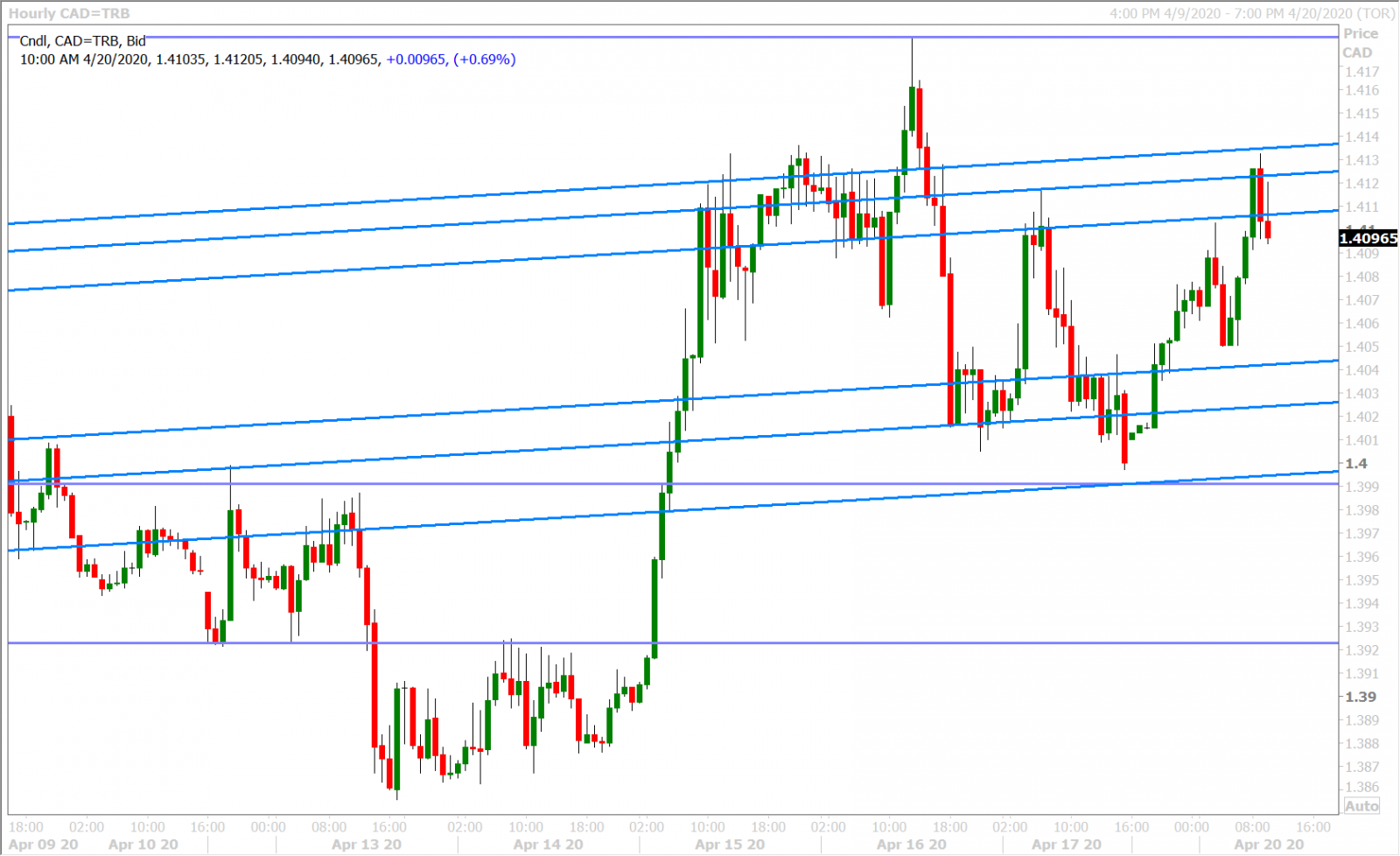

Retail oil investors have been learning what “contango” means after the US Oil Fund (USO), which accounts for almost 25% of all outstanding WTI futures contracts, was forced to change its exposure from holding 100% of the front month future to 80% front month/20% second month. This was in response to a tripling in assets under management for the popular retail oil market-proxy during the last six weeks and led to a sloppy May/June futures rollover last week. When we combine this financial market dynamic with the fact that physical oil storage is becoming increasingly more difficult to find, we’re seeing a complete capitulation from traders who don’t want to take delivery of the May contract which expires tomorrow. The 40% plunge in the May contract is stealing all the headlines this morning; is leading to an 12% decline in the June contract, and is the primary driver behind USDCAD’s swift rise back to the 1.4100-1.4120 resistance band. The broader USD has completely erased its early morning losses in Europe and is now trading higher as the crude oil plunge starts to hit equity market risk sentiment (S&Ps -2%).

The latest Commitment of Traders report from the CFTC showed little change to the leveraged fund net long position in USDCAD during the week ending April 14; a fitting development quite frankly, given the market’s neutral chart structure for the month of April so far. This week’s economic calendar will feature some stale Canadian data (February Retail Sales and March CPI) but we will get some fresh employment and business sentiment figures out of the US on Thursday (Jobless Claims for the week ending April 11 + April Flash PMIs). We’ve now entered the traditional blackout period ahead of the Fed’s next policy meeting on April 29.

USDCAD DAILY

USDCAD HOURLY

MAY CRUDE OIL DAILY

EURUSD

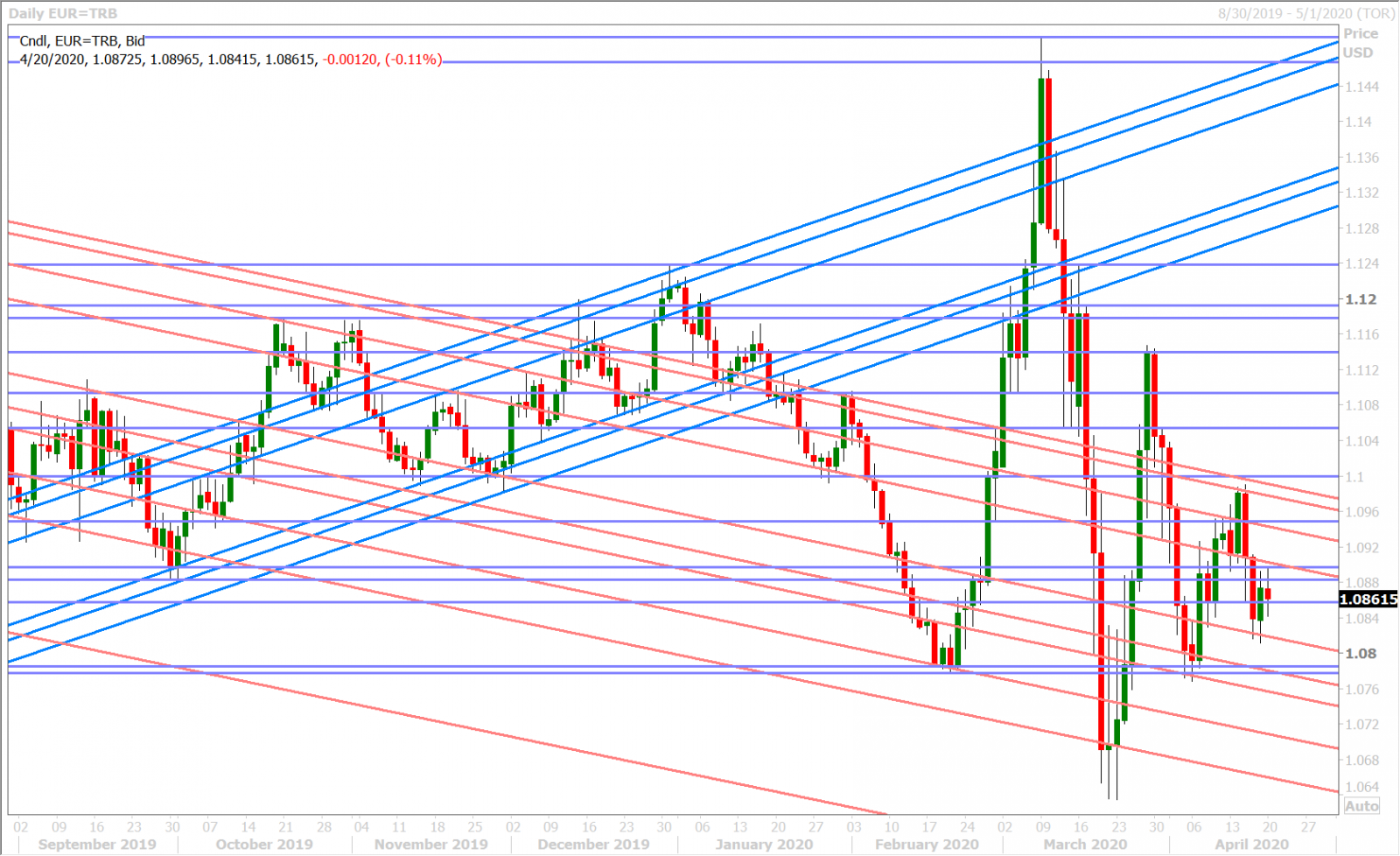

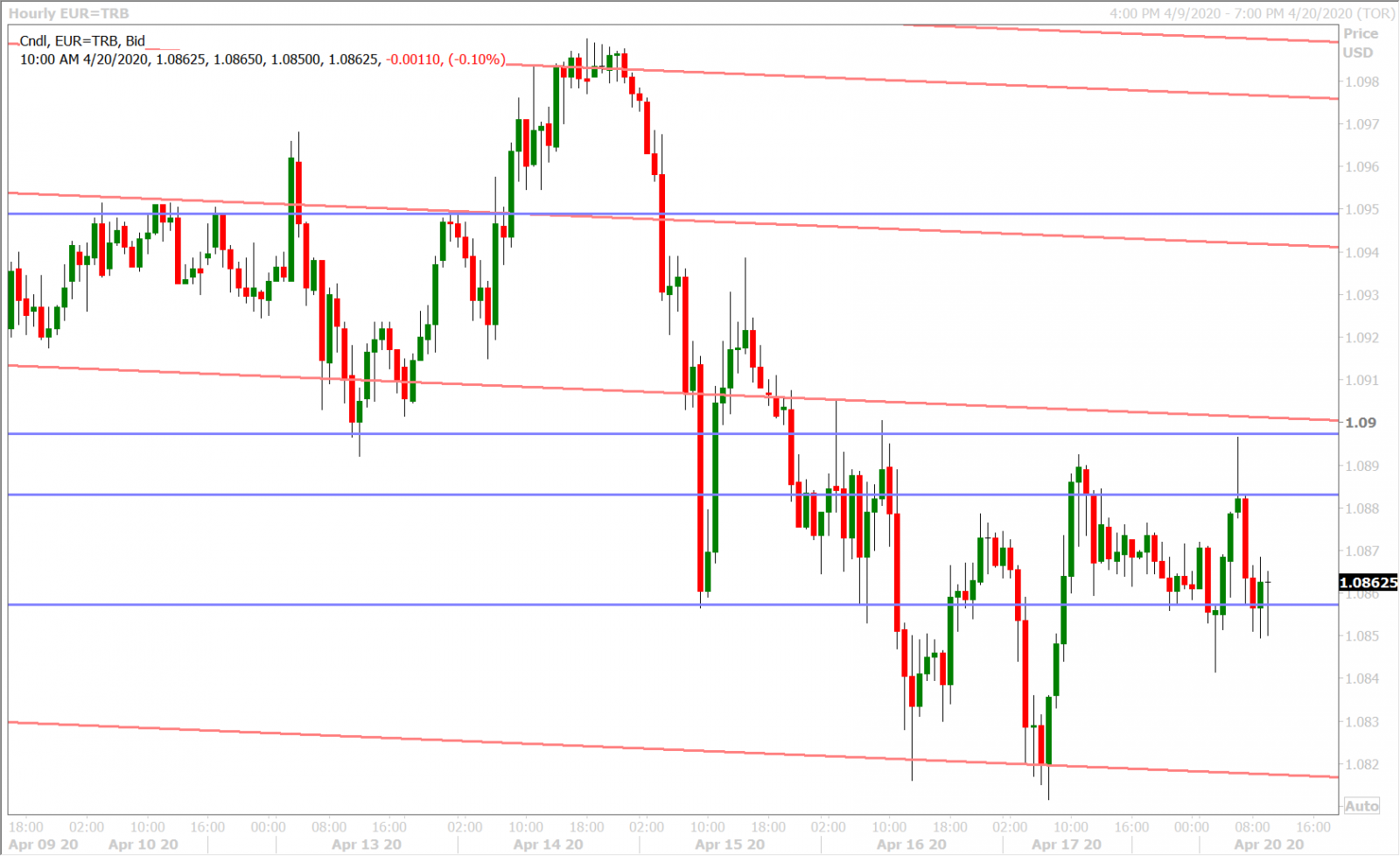

Euro/dollar price action has been a bit messy to start out the week. Friday’s lackadaisical NY close between the 1.0850s and the 1.0880s didn’t help, nor did a relatively subdued Asian session last night in terms of news flow. European stocks initially opened higher this morning, but have since retreated with oil prices and another widening of the BTP/Bund spread. Broad USD safe-haven buying flows appear to be the driver of EURUSD at this hour, but we cannot say that the market is definitively breaking down. We wouldn’t be surprised to see a bit more range trading here ahead of this week’s EU Summit, where it is likely Italian Prime Minister, Giuseppe Conte, will continue to push for the issuance of “coronabonds”.

The latest Commitment of Traders report from the CFTC showed the leveraged funds increasing their net long EURUSD position for the 4th week in a row during the week ending April 14; not a great development given the market’s swift move back below the 1.10 level so far this month. We think last week’s upside rejection of the 1.0980s (close enough to the 1.10s) was also quite discouraging for the EUR bulls as it puts renewed focus on chart support levels in the high 1.07s/low 1.08s. Traders will have plenty of fresh April economic sentiment data to chew on this week (see below):

Tuesday: German ZEW Economic Sentiment (-42.3 exp)

Thursday: German Flash PMI (31.0 exp) and Eurozone Flash PMI (25.7 exp)

Friday: German IFO Expectations Index (75.0 exp)

EURUSD DAILY

EURUSD HOURLY

SPOT GOLD DAILY

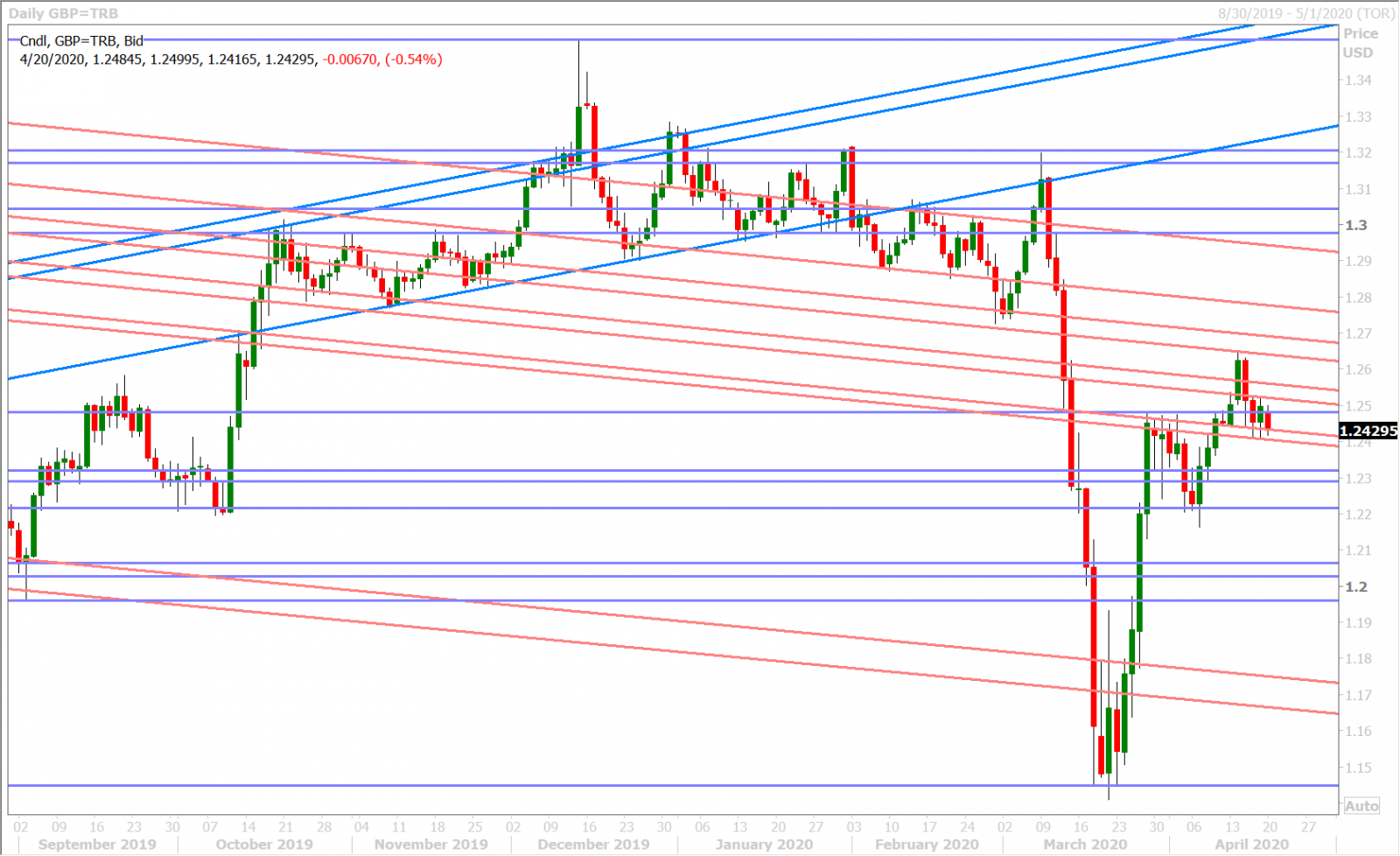

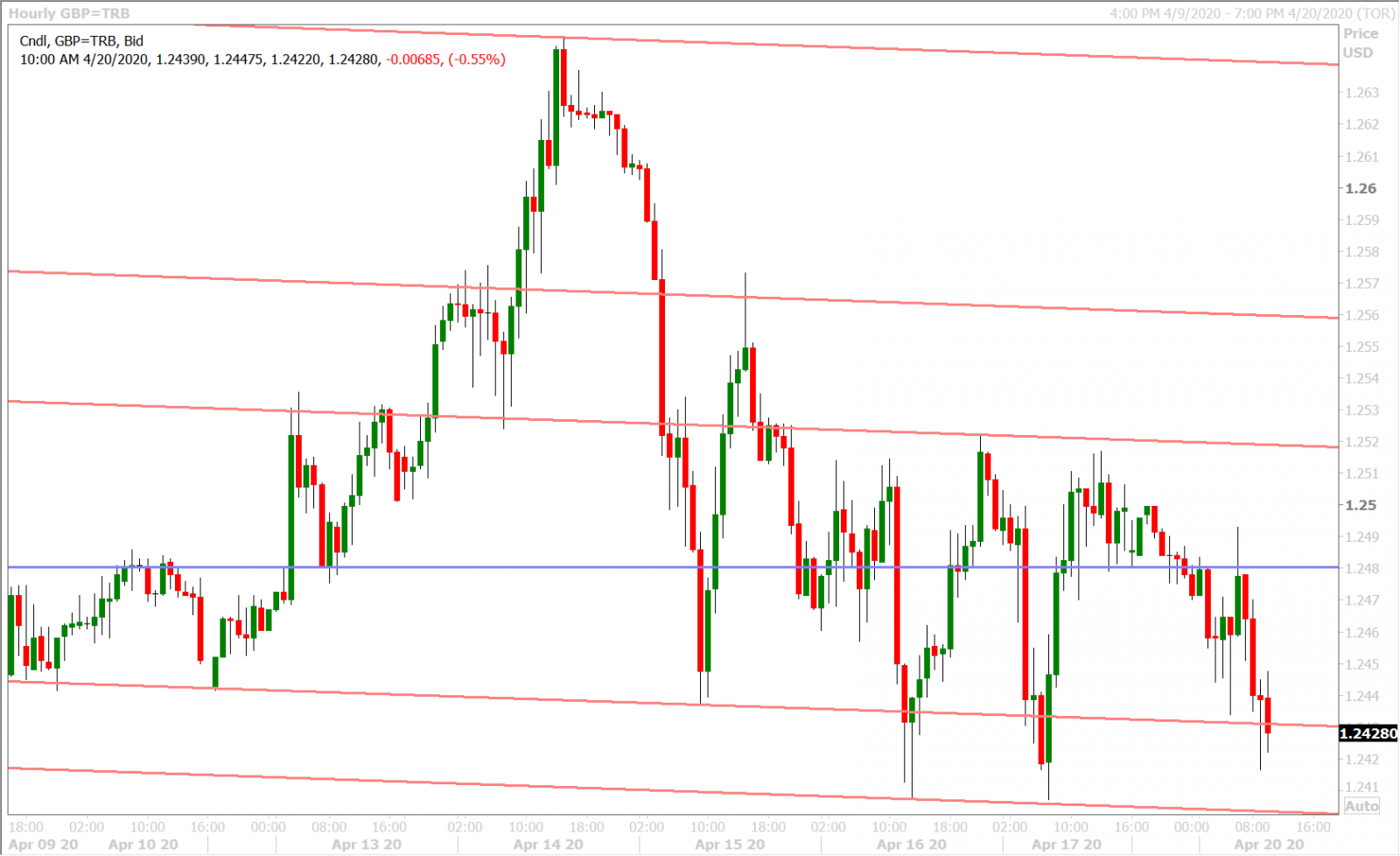

GBPUSD

Sterling is not giving traders much to work with this morning as it largely remains confined to the 1.2430-1.2520 range we talked about last week. Over 2.8blnEUR in options expire at the 0.8700 strike in EURGBP this morning, which could help GBPUSD bounce. Aside from that, sterling should trade with the broader USD tone, as it has done of late.

The latest Commitment of Traders report from the CFTC showed very little change to the tiny net long GBPUSD position held by the leveraged funds; which is not surprising considering the market's muted volatility for April. This week’s UK economic calendar will feature a bunch of stale figures (February Employment, March CPI, March Retail Sales) but we’ll get the flash PMIs on Thursday, which will give us a fresh look at UK business sentiment for April.

GBPUSD DAILY

GBPUSD HOURLY

EURGBP DAILY

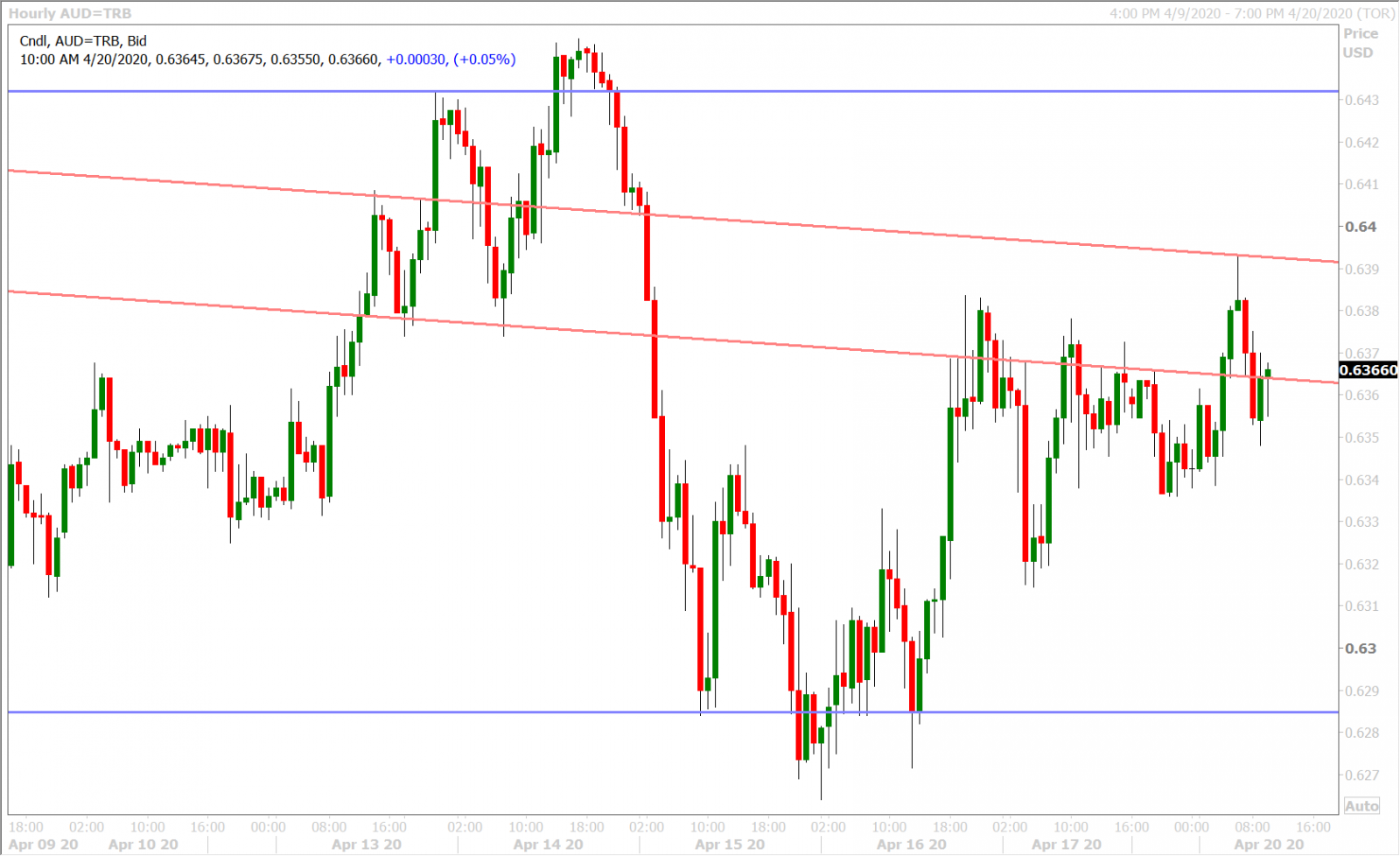

AUDUSD

The Australian dollar is showing some relative out-performance versus its G7 peers this morning and we’re hearing that New Zealand’s plan to reopen their economy next week is one of the reasons why. We wouldn’t put too much stock into this narrative, and while AUDUSD is enjoying modest gains across the board at this hour, it continues to toy with both sides of the pivotal 0.6360s level we talked about last week.

This is hardly an expression of directional bias and leaves the market with a more range-bound tone in our opinion heading into Phillip Lowe’s speech tomorrow. The RBA Governor is expected to give an “economic and financial update” at 1amET tomorrow morning. Australia will release its April flash PMI data on Wednesday night ET.

AUDUSD DAILY

AUDUSD HOURLY

USDCNH DAILY

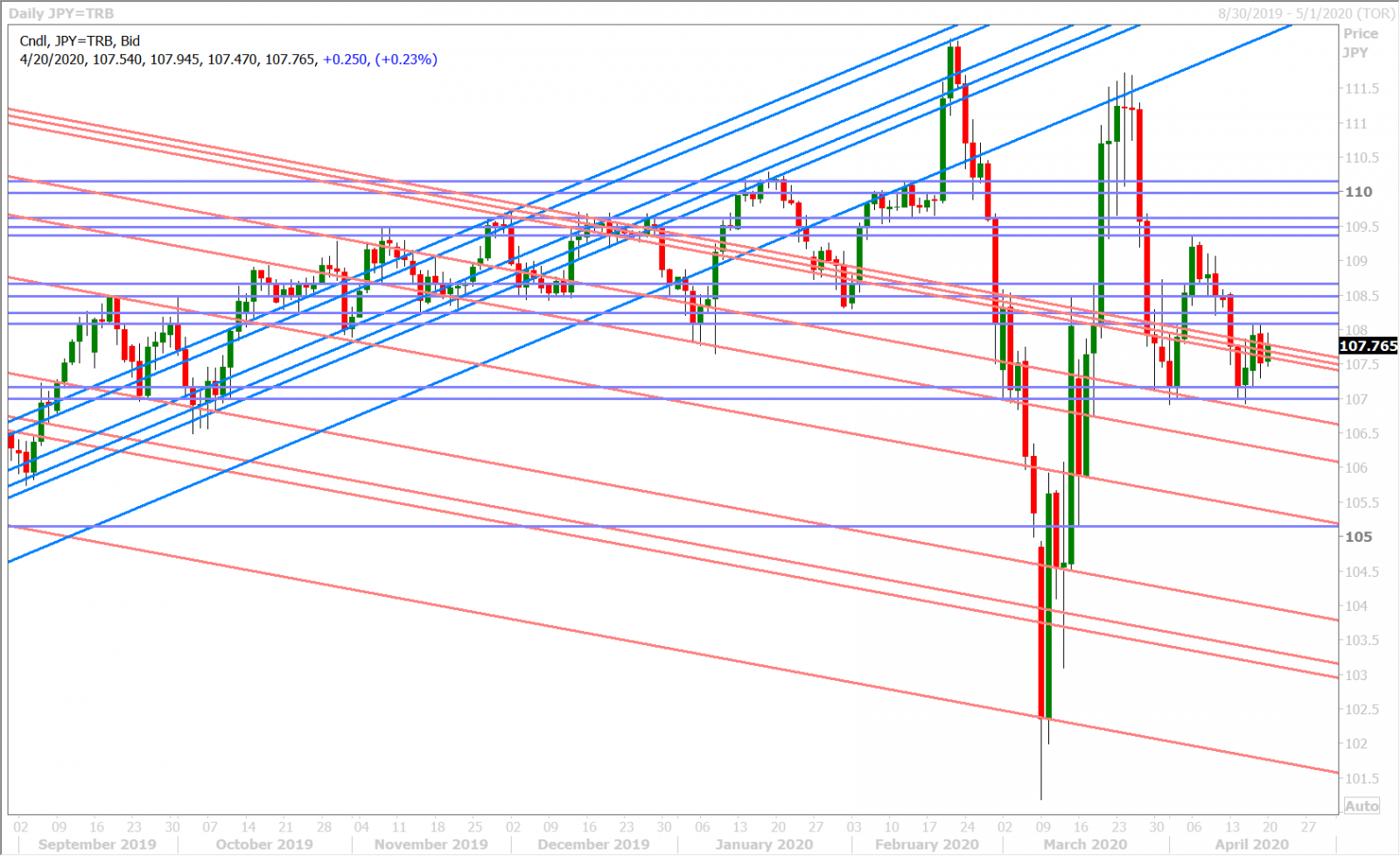

USDJPY

Dollar/yen has started the week with a non-directional tone, but it appears the USD is slightly winning the battle of the safe-havens this morning as USDJPY trades with an inverse correlation to the broader risk tone. The 107.50-70 support zone (formally the 107.60-80s because of the downward sloping nature of the trend-lines that created it), is proving to be a familiar battleground once again.

Last night’s Japanese Trade Balance release for March showed exports falling at the fastest pace since July 2016 (-11.7% YoY vs -10.1% exp). The latest Commitment of Traders report from the CFTC showed barely any change to the leveraged fund net short USDJPY position during the week ending April 14.

USDJPY DAILY

USDJPY HOURLY

US 10 YR YIELD DAILY

Charts: Reuters Eikon

About the Author

Erik Bregar - Director, Head of FX Strategy

Erik works with corporations and institutions to help them better navigate the currency markets. His desk provides fast, transparent, and low cost trade execution; up to the minute fundamental and technical market analysis; custom strategy development; and post-trade services -- all in an effort to add value to your firm’s bottom line. Erik has been trading currencies professionally and independently for more than 12 years. Prior to leading the trading desk at EBC, Erik was in charge of managing the foreign exchange risk for one of Canada’s largest independent broker-dealers.

Interested in creating a custom foreign exchange trading plan? Contact us or call EBC's trading desk directly at 1-888-729-9716.

Exchange Bank of Canada, EBC – Canada’s Foreign Exchange Bank, is the only Schedule 1 Canadian bank specializing in foreign currency exchange and international payments for financial institutions and corporations. EBC provides innovative foreign exchange management and integrated international payment solutions tailored to meet business needs on a global scale. Leveraging industry leading technology and a client-focused team of experts EBC delivers comprehensive, cost-effective and trusted payment processes and foreign exchange currency solutions to create financial and operational efficiencies. To learn more, visit: www.ebcfx.com.