USDCAD bid. EUR mixed as net longs hit 10yr high. Options in play in AUD and GBP near term.

Summary

-

CME OPEN INTEREST CHANGES 12/15: AUD -5007, GBP +13677, CAD +6383, EUR +37795, JPY -6746

-

CFTC COMMITMENTS OF TRADERS REPORT (NET SPECULATIVE POSITIONS AS OF DEC 12). AUDUSD open interest shot up considerably as the market made new swing lows, but seeing as longs and shorts added almost the same amount, the net long AUDUSD remains largely unchanged week over week. Position liquidation was the theme in GBPUSD during the volatile week ending Dec 12. Shorts liquidated a little bit more than longs, making the net GBPUSD position slightly longer for the third week in a row. Traders liquidated in USDCAD too, with longs and shorts trimming almost the same amount, leaving the net USD short (CAD long) pretty much unchanged week over week at +42k contracts. The fact there wasn't much net position change or open interest change here for the second week in a row despite the 200 point bounce higher in USDCAD shows a lack of new participation and a market of entrenched positions that continue to view this market as range-bound. The net EURUSD long position shot up to a 10yr high in the week ending Dec 12, largely on the back of massive covering from shorts as the market leaked 100 points lower going into the Fed and ECB meetings last week. The net USD short (JPY long) position was largely unchanged as both longs and shorts liquidated moderately in equal amounts, and this was despite the technical breakout back above 113.

-

ECONOMIC CALENDAR FOR THE WEEK: The week ahead will be relatively quieter compared to last week, as markets wind down for the Christmas holidays. There is nothing notable on the calendar today. TUESDAY: Australian RBA Dec Rate minutes, German IFO for Dec, US Housing Starts, WEDNESDAY: US Existing Home Sales, THURSDAY: US Philly Fed survey, Canadian CPI and Canadian Retail Sales, Final read on US Q3 GDP, FRIDAY: Final read on UK Q3 GDP, Canadian Oct GDP, US PCE Index, US Durable Goods.

-

UPCOMING CENTRAL BANK SPEAK: BOE’s Governor Carney speaks in Parliament on Wednesday. Bank of Japan announces its monetary policy update on Thursday with a press conference from Kuroda afterwards.

-

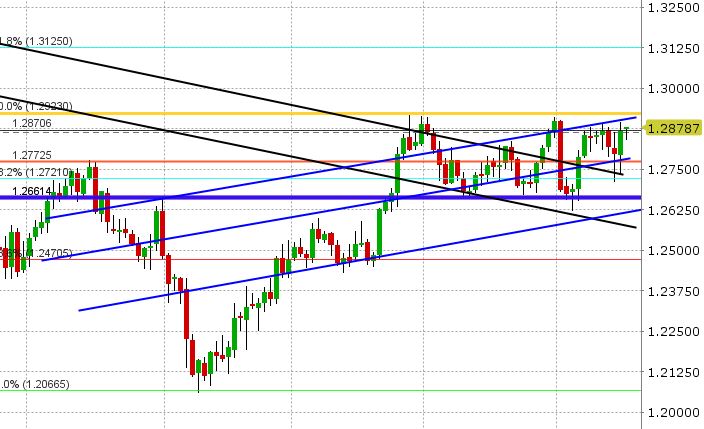

USDCAD: Dollar/CAD staged an important recovery during NY trading on Friday, with the market regaining key support in the 1.2760-70s and then some. A broad USD bid lifted all boats and the weaker than expected read on Canadian Manufacturing Sales for October, while not key economic indicator for traders, was a nice backdrop for USDCAD bulls. USDCAD is starting the week in good shape technically as the market is bumping up against familiar resistance (1.2870-1.2900). The US/CA 2yr yield spread has firmed back to +30bp. EURCAD and GBPCAD are being bought, with the former now effectively cancelling out Thursday’s bearish outside day and the latter regaining 1.72 after Friday’s inverted hammer reversal. So everything’s going right for USDCAD at the moment. While the week ahead will be quieter in terms of economic data from rest of the world, we have three important Canadian data points out later in the week (CPI, Retail Sales, GDP). Traders are now talking about what lies above the 1.2920s on the charts (ie. stops, option barriers). Traders are also talking about a piece from the Globe & Mail on the weekend, quoting the BOC’s Stephen Poloz and how he’d like to get markets used to a lack of detail surrounding forward guidance as markets return to “normalcy”.

-

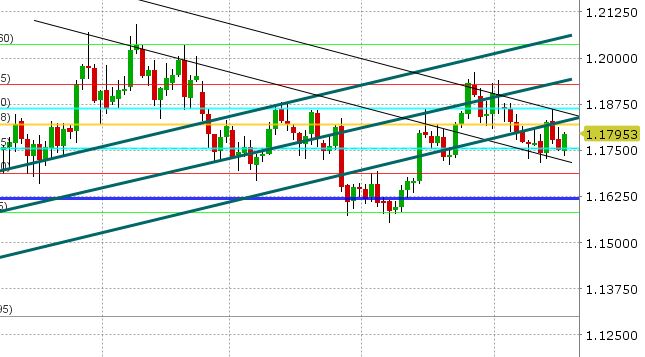

AUDUSD:The Aussie continues to consolidate recent gains, sitting comfortably in the 0.7640-0.7670 range. Friday’s broad USD rally didn’t hurt the chart too much as weekly support in the 0.7630-0.7640s held. Copper and other base metal prices continue to charge higher, which is a positive backdrop for AUDUSD, and the AU/US 2yr yield spread is up-ticking closer to +10bp again. Beside the RBA’s minutes tomorrow, it will be a quiet week for Australian data. Reuters is reporting a huge option expiry (2bln+ AUD) at 0.7700 on Friday.

-

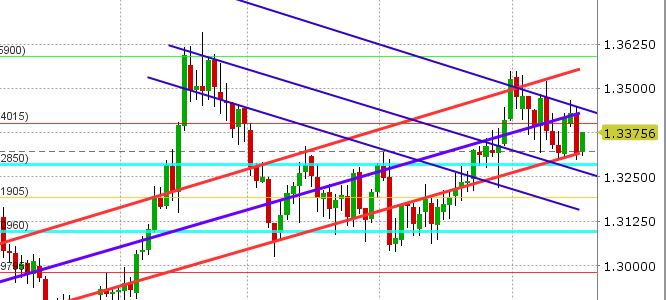

EURUSD: Traders are talking about the new 10yr high in the net EURUSD long futures position, reported by CFTC late Friday. While it would suggest that bullish market sentiment is overcrowded here given recent price action, we would note that the reduction of short positions (that caused this new high in net positioning) was absorbed by new short positions in the “small speculator” portion of the CFTC’s report (this category of positioning is less followed). In other words, the short position from the big spec funds got “re-allocated” to small specs and at the end of the day overall open interest didn’t go down week over week. So we’re taking the CFTC news with a grain of salt. We’re also hearing some talk this morning of a new head & shoulders (H&S) topping pattern in EURUSD (see chart). We feel it’s a legitimate pattern, especially considering the market is below the 50% Fibo of the Sep-Nov downmove, and below trend-line support in the low 1.18s, but there’s not enough force behind it yet. There’s still plenty of support in the 1.1720-1.1750 area. Option expiries continue to abound and attract attention of late. Plus we have renewed support from EURGBP, which made an important low last week (Sunday opening gap from June 2016 filled). We feel EURUSD is going to be a bit of a mixed bag here as markets wind down for the holidays.

-

GBPUSD: Sterling nosedived on Friday as the EU summit came and went without any new positive headlines regarding Brexit negotiations, and with that GBPUSD chart took a dent. With Friday’s poor close, GBPUSD is now at risk of attacking the 1.32s. GBPUSD is rallying now, desperately trying to reduce the chances of that possibility, but if the market were to once again test trend-line support at 1.3325, we feel the floor might give out next time. Today’s action might also be influenced by a widely reported option expiry at 1.3350 this morning for over 2bln GBP. We continue to call GBPUSD range-bound but are cognoscente of Friday’s poor trading pattern.

Market Analysis Charts

USD/CAD Chart

AUD/USD Chart

EUR/USD Chart

GBP/USD Chart

Charts: TWS Workspace

About the Author

Erik Bregar - Trader

Erik works with corporations and institutions to help them better navigate the currency markets. His desk provides fast, transparent, and low cost trade execution; up to the minute fundamental and technical market analysis; custom strategy development; and post-trade services -- all in an effort to add value to your firm’s bottom line. Erik has been trading currencies professionally and independently for more than 12 years. Prior to leading the trading desk at EBC, Erik was in charge of managing the foreign exchange risk for one of Canada’s largest independent broker-dealers.

Interested in creating a custom foreign exchange trading plan?

Exchange Bank of Canada (EBC) is a Schedule 1 bank based in Toronto, Canada. EBC specializes in foreign exchange services and international payments providing a wide range of services to financial institutions and corporations, including banknote foreign currency exchange, travelers' cheques, foreign currency cheque clearing, foreign currency bank drafts, Global EFT and international wire transfers through the use of EBC's innovative EBCFX web-based FX software www.ebcfx.com.